About the Author: Fahad Nawaz is a Multan based Researcher compiling authentic sources from sahih Bukhari, Tirmidhi, and scholars like Ibn Taymiyyah.

For questions about this article or to suggest updates, contact: [email protected]

When you want to learn about murabaha, you usually find either sterile banking pamphlets or encyclopedia entries with zero Quranic evidence. This gap isn’t trivial, because murabaha is the most widely used Sharia-compliant financing tool across the globe, yet its validity depends on conditions that most explanations fail to describe.

Murabaha (مرابحة) is a sale that is Sharia-compliant: a bank buys an asset, and later sells it to the buyer at a profit margin that is clearly explained and paid in instalments. Unlike traditional loans, no riba (interest) is charged in murabaha. All four Sunni madhabs permit it under specific conditions, making it the single most widely used Islamic financing tool.

Note: The views of scholars can vary; this guide presents the mainstream Sunni scholarly positions.

What most resources fail to mention is the tension at the heart of murabaha: even those scholars who support its legality, such as Mufti Taqi Usmani himself, refer to it as a borderline transaction and an intermediary stage towards profit-and-loss sharing. That tension changes how you should evaluate any murabaha product you encounter.

By the end of this guide, you’ll know the five Shariah conditions that make a murabaha contract valid, the Quranic and Hadith evidence foundation supporting each, and how the four madhabs interpret them differently, but also how providers like Devon Bank design murabaha home financing in thirty-four states of the United States. You’ll also get an original eight-point compliance checklist to independently verify any murabaha product.

Every claim below is sourced from Quranic tafsir (Ibn Kathir and al-Qurtubi), authenticated Hadith (Sahih al-Bukhari and Sunan Abu Dawud), classical fiqh works (al-Mughni and al-Hidayah), and the latest 2025–2026 AAOIFI reform publications.

What Is Murabaha? The Plain-English Meaning Behind the Arabic

The word murabaha (sometimes written murabahah or murābaḥah) is derived out of the Arabic root ر-ب-ح that produces ribḥ (ربح) — meaning profit. Murabaha is a type of sale contract in the lexicon of fiqh al-muʿāmalāt (Islamic commercial jurisprudence): the buyer and seller agree that the price of an asset will be a cost plus a markup: the seller openly reveals the cost of the asset and marks up the price.

Through that Arabic root, there is a difference that most guides do not see. The two notions of ribḥ (profit through active trade) and riba (profit through passive lending of money under the Islamic law) are fundamentally different. The first one is permitted; the second one is haram. Ribḥ is obtained by being directly involved in economic activity, that is, by buying, holding, bearing risk and selling thereof, and riba is obtained as a result of the time passing of owed money.

This line is clearly outlined in the Quran:

ٱلَّذِينَ يَأۡكُلُونَ ٱلرِّبَوٰاْ لَا يَقُومُونَ إِلَّا كَمَا يَقُومُ ٱلَّذِي يَتَخَبَّطُهُ ٱلشَّيۡطَٰنُ مِنَ ٱلۡمَسِّۚ ذَٰلِكَ بِأَنَّهُمۡ قَالُوٓاْ إِنَّمَا ٱلۡبَيۡعُ مِثۡلُ ٱلرِّبَوٰاْۗ وَأَحَلَّ ٱللَّهُ ٱلۡبَيۡعَ وَحَرَّمَ ٱلرِّبَوٰاْۚ

“Those who consume interest cannot stand [on the Day of Resurrection] except as one stands who is being beaten by Satan into insanity. That is because they say, ‘Trade is [just] like interest.’ But Allah has permitted trade and has forbidden interest (riba)…”

(Surah Al-Baqarah, 2:275)

Ibn Kathir understands this verse as the main rule of dividing the lawful commercial gain and the unlawful interest. Preeminent contemporary expert on Islamic finance, Mufti Taqi Usmani has maintained that the term permitted trade is inclusive of credit sales like murabaha whereas the term forbidden usury is exclusively related to extra charge of late payments or lending money with interest.

Murabaha as such therefore, is not a loan; it is a sale, the cost and the profit being exposed to the buyer to view, to approve or disapprove.

What makes murabaha unique among Islamic sales — and why critics call it a ‘borderline transaction’ — is that the buyer typically doesn’t pay the full price at once. It’s the deferred payment structure that fuels the scholarly debate.

How Murabaha Actually Works: A Step-by-Step Breakdown Anyone Can Follow

Stripped of the jargon, a murabaha transaction has six steps. Take a practical example: a real-life house buying — the situation most of the readers are concerned with.

Step 1 — The Buyer Identifies the Asset

You find the property (or vehicle, or equipment) that you want to purchase, do due diligence, negotiate with the seller on the price, just as you would in any other transaction. No financing is yet arranged.

Step 2 — The Buyer Approaches the Islamic Bank

You visit an Islamic bank or other financial institution to ask them to give you murabaha financing. You provide the description of the product, its value, and the supplier. This is where you can do a waʿd (purchase promise), which is binding or not, according to the madhab and school, a promise that you are serious and therefore can lead to a deal.

Step 3 — The Bank Purchases the Asset

This is the point of difference between murabaha and a traditional loan. The financier buys the asset at the supplier level and pays the seller the full price taking possession of the asset. As the Prophet ﷺ stated:

“Do not sell what you do not own.”

(Narrated by Ḥakim ibn Ḥizam, Sunan Abu Dawud, Hadith No. 3503, Sahih)

The bank cannot simply transfer money to you but it must first become the owner of the asset itself.

Step 4 — Ownership Transfers to the Bank

The bank carries all ownership risk from the moment it acquires the asset until it sells it to you. If the property is damaged, destroyed, or found to have defects, the loss falls on the bank — NOT yours. This true risk-taking is a fundamental Sharia-based aspect that differentiates murabaha and a veiled loan.

Step 5 — The Bank Resells to the Buyer at Cost + Profit

During this phase the financial intermediary will sell the asset to you at a price which includes the original cost as well as a profit margin, the latter being entirely transparent. An example of this is the Devon Bank which is run on the basis of Islamic principles and offers a fixed purchase price that the customer pays over an extended term without any extra interest. The total price combines what Devon Bank paid and the bank’s profit.

An actual numerical example is as follows: Devon Bank (Devon Islamic) buys a condominium in the amount of US $240,000 and later sells it to the buyer in installments of 15 years of payment of US $1,586.21 each month. The markup of US $46,000 forms a profit rate of 2.375% APR that is not interest since it was as a result of a bona fide sale and not a loan of money.

Step 6 — The Buyer Pays in Agreed Instalments

The total amount agreed is settled in the form of fixed monthly instalments. The purchase price remains fixed — even if you make early or advance payments. The financier may, at its discretion, forgive part of the remaining balance. More importantly, there is no compounding, no variable rate and no adjustment associated with benchmark interest rates.

يَٰٓأَيُّهَا ٱلَّذِينَ ءَامَنُوٓاْ إِذَا تَدَايَنتُم بِدَيۡنٍ إِلَىٰٓ أَجَلٖ مُّسَمّٗى فَٱكۡتُبُوهُۚ

“O you who have believed, when you contract a debt for a specified term, write it down. And let a scribe write [it] between you in justice…”

(Surah Al-Baqarah, 2:282)

This verse establishes the Shariah principle that all financial dealings must be documented in writing — ensuring that every term of a murabaha agreement is recorded.

At this point, having understood the mechanics, you are likely to ask: why is this type of sale regarded as halal when it resembles the way a conventional loan? The answer lies on five fundamental conditions that are considered by all the scholars of madhabs as indispensable.

The 5 Shariah Conditions That Make or Break a Murabaha Contract

Failure to meet any of these conditions causes the transaction of murabaha to become haram, fasid (voidable), or batil (void). Such are not discretionary principles, but structural requirements which are based on hadith and classical fiqh.

Condition 1: The Bank Must Actually Own the Asset First

The Sunnah scholars treat this as a non-negotiable condition: the bank must take possession of the property in full, and then sell it to the purchaser. The hadith is explicit:

“Do not sell what you do not own.”

(Narrated by Ḥakim ibn Ḥizam, Sunan Abu Dawud, Hadith No. 3503, Sahih)

If the bank lacks actual title and merely facilitates a money transfer, this breaches the condition, and the transaction takes the form of a disguised interest-bearing loan.

Condition 2: The Bank Must Take Genuine Possession (Qabd)

It is not sufficient to have paper-legal title. Much instruction in the Quran and in what the Prophet taught emphasizes the need of actual possession:

“When you have bought something, do not sell it before you have taken possession of it.”

(Narrated by Ḥakim ibn Ḥizam; Musnad Ahmad, Hadith No. 15399; Sunan al-Nasaʾi, Hadith No. 4613, authenticated by Sheikh al-Albani)

This fact is strengthened by the narration of a companion: the Prophet ﷺ did not allow selling goods in the same place where they were bought and then transferred by traders to their own place (Sunan Abu Dawud, Hadith No. 3499). This regulation discourages murabaha transactions that involve paper only where no change of hand of the asset actually occurs.

Condition 3: Cost Price and Profit Margin Must Be Disclosed

The characteristic of murabaha is transparency. The original cost price must be communicated to the buyer and the exact profit margin communicated. In case the price is hidden, the classical scholars consider the contract voidable. This is what makes the difference between murabaha and a plain sale (musawamah), the latter being where the seller has no obligation to disclose expenses.

Condition 4: The Price Once Fixed Cannot Change

Once the price in the form of murabaha is fixed, it cannot be lowered so as to pay early or raised in the case of default. There is no price fluctuation allowed and the fixed-price institution is one of the most powerful barriers against riba — there is no compounding, no adjustable rate, no penalty interest.

Condition 5: The Underlying Asset Must Be Halal and Existent

The goods must be halal, existent, owned by the seller, and in the seller’s possession at the time of sale. They must be specifically identified and deliverable with certainty. The murabaha deal cannot be made based on liquor, pork, or even future hypothetical commodities.

At this stage most expositions stop. However, scholars across the four madhabs differ on how some of these conditions apply in practice — and those differences matter when you’re evaluating a specific murabaha product.

For practical guidance on verifying whether goods meet halal certification standards, consult our verification guide.

What Do the Four Madhabs Really Say About Murabaha?

Mufti Taqi Usmani observes that the sale of credit which is the essence of the murabaha has unanimous consensus among the four Sunni schools of the Islamic law and most of the Muslim jurists. They agree on the principle of permissibility; they differ on the procedural details.

The four madhabs disagree over several practical issues: Does the original promise (waʿd) of the buyer hold? Is the buyer able to be the agent of the bank (wakala) and to purchase the asset on behalf of the bank? What is considered to be adequate qabd (possession)? Is it allowable to have early-payment discounts?

| Madhab | Position on Murabaha | Primary Evidence | Classical Authorities | Key Conditions Emphasized | Contemporary Fatwa Support |

| Hanafi | Permissible as a sale contract subject to conditions | Quran 2:275; Hadith on credit sales | Imam Abu Hanifa; al-Hidayah; Badaʾiʿ al-Sanaʾiʿ (al-Kasani) | Disclosure of cost and profit; buyer knowledge; lawful purchase | Darul Uloom Deoband; Mufti Taqi Usmani |

| Maliki | Permissible; emphasizes transparency and no deception (ghish) | Quran 2:275; transparency in trade | Imam Malik; al-Mudawwana | Full disclosure; no concealment of defects | Dar al-Ifta al-Misriyyah |

| Shafiʿi | Permissible; categorised as bayʿ al-amanah (trust sale) | Quran 4:29; reliance on disclosure | Imam al-Shafiʿi; al-Umm; Imam al-Nawawi; al-Majmuʿ | Mutual consent; transparent cost-plus structure | Al-Azhar Fatwa Committee |

| Hanbali | Permissible under strict ownership conditions | Abu Dawud 3503; Ahmad 15399 | Imam Ahmad ibn Hanbal; Ibn Qudamah; al-Mughni | Real ownership transfer; genuine possession (qabd) | Sheikh Ibn ʿUthaymeen; Islamic Fiqh Academy Jeddah |

Each position is supported by strong evidence. Readers are encouraged to follow the qualified scholars of their respective madhab.

The Hanbali stance is especially educative. Ibn Qudamah writes in al-Mughni, that any loan where it is said that above the original amount must be returned is haram and there is no difference among the scholastic opinion. This rigid division between qard (loan) and bayʿ (sale) is the very reason why the Hanbali school insists most on real transfer of ownership, otherwise the transaction will not be a sale but a loan at a markup, which is riba.

Since all the madhabs concurred that it is permissible, then why do some scholars continue to declare that murabaha is undesirable? The answer reveals a significant tension in modern Islamic finance.

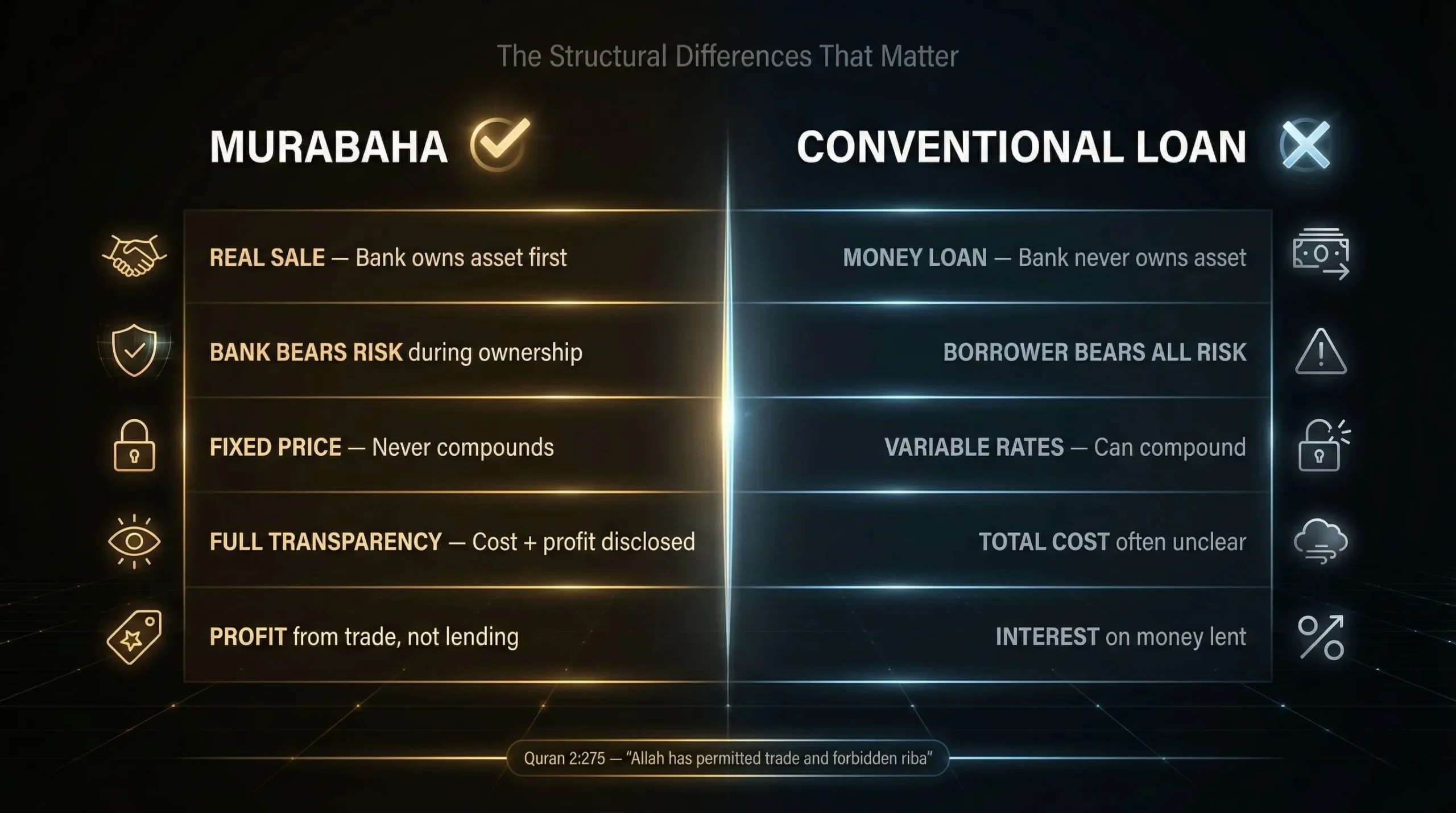

Murabaha vs. Conventional Loans: Why They’re NOT the Same (Despite What Critics Say)

The objection to the single most prevalent murabaha is as follows: “The bank imposes a markup which appears to be interest. The monthly payments appear similar. So how is it any different?” Critics observe that in reality, most murabaha deals are simply cash-flows among banks, brokers and borrowers with the financial perspective being the same as traditional financing. This criticism deserves a thorough response.

| Feature | Murabaha | Conventional Loan |

| Profit/Interest | Seller is entitled to a religiously acceptable profit on sales of goods | Lender charges interest on money lent |

| Ownership | Seller/financier has to assume responsibility and take physical possession; bears risk of defective goods | Lender never owns the asset |

| Price | Fixed when it is created; unable to change | Variable or fixed interest rate; total cost often unclear |

| Late Penalty | The bank is unable to charge interest; debated late payment fees; some scholars argue they should be given to charity | Compounding interest and penalty fees apply |

| Asset Requirement | Must be a real, tangible asset/commodity | Money-for-money |

| Transparency | Full cost plus profit reported | Interest rate reported; total cost is not generally clear with variable rates |

The prohibition of riba is part of Islam’s broader framework against unjust enrichment, which also covers gambling and lottery.

Mufti Taqi Usmani answers the criticism in the most straightforward way: the price is on the commodity and not against money, and thus it is not forbidden in Islam. The structural differences are not cosmetic. The bank is facing real ownership risk. The price does not compound and is fixed. And the exchange is one of real property, not the issuance of loans.

With that said, the academic community is also aware of a valid concern. Even scholars who advocate Islamic finance view murabaha as a transitional step — an acceptable but not ideal mode of financing on the road toward genuine profit-and-loss sharing. The Council of Islamic Ideology has termed murabaha as no more than second best solution and even Mufti Taqi Usmani has termed it as a borderline transaction.

The Shariah point of view is that scholars tend to prefer equity-based contracts like mudarabah and musharaka (partnership) as compared to debt-based contracts like murabaha. The fiqh principle of sadd al-dharaʾiʿ (blocking the means to harm) underlies the fact that: the structural similarity of murabaha and interest-bearing loans may become a portal to riba unless the terms and conditions are strictly adhered to.

It is one thing to understand the theory. However, what does murabaha actually look like in practice — e.g. when you are buying a United States home?

Murabaha Home Financing in the USA: Your Real-World Options in 2026

Getting a halal Islamic mortgage in the USA is easier than ever and several established providers provide Shariah-compliant home financing in the country. Murabaha, ijara (lease-to-own) and musharaka (diminishing partnership) are the three large models applied in the West. Each has its own advantages.

Devon Bank Murabaha — How It Works in Practice

Devon Bank (Devon Islamic) has been offering financing which is halal since 2003 and is now offering murabaha home financing in 34+ states in the U.S., including California, Texas, Illinois, Florida, New York, and Virginia.

Here’s how Devon Bank structures it: Devon Bank never lends any money. Rather it buys at your discretion and sells the property to you at an agreed price. On closing you do not sign a promissory note with principal and interest rate. Rather you enter into a contract of murabaha of the amount of the balance to be paid.

Prepayment is an issue to be taken seriously. When a contract on murabaha has been signed, the price is not changeable. The financier may, at its discretion, forgive part of the remaining balance, however, a reduction in advance is not acceptable under the conditions of a murabaha contract.

Devon Bank’s documents are prepared in consultation with local religious authorities and with authorization of the Shariah Supervisory Board of America, guided by Mufti Nawal-ur-Rahman.

Murabaha vs. Musharaka vs. Ijara — Which Islamic Mortgage Is Right for You?

Musharaka (diminishing partnership) has emerged as the most popular Islamic mortgage structure used in the U.S. since it fits within U.S. mortgage regulatory frameworks while remaining Shariah-compliant. Partnership also permits property rights and title registration.

Although it is an acceptable contract, a murabaha is disadvantageous because it is deemed to be like a debt. Due to this reason, some providers in the United States do not consider the murabaha financing as a preferred model. Nonetheless, there are non-Muslim clients who take Islamic financing specifically due to the fact that they are more comfortable with the certainty of the fixed price of murabaha, which is no variable rates, no surprises.

The most ideal model will be based on your priorities: Are you interested in fixed pricing certainty (murabaha), or the flexibility of rental (ijara), or equity partnership (musharaka)?

Other USA Providers Offering Murabaha or Shariah-Compliant Mortgages

In addition to Devon Bank there are other institutions that cater to the American Muslim community:

Guidance Residential with the predominant use of the musharaka framework is one of the leading mortgage providers of Islamic finance in the United States.

The UIF Corporation offers a wide range of financing solutions that comply with Shariah.

Being one of the first players in the American Islamic finance industry, Lariba still provides innovative solutions.

Minnwest Bank is a provider of Islamic financing products with growing market presence.

The murabaha product offered by Citywide Home Mortgage is defined by custom-made documentation, which is supported by a fatwa to meet the requirements of the Shariah laws. The buyer will make monthly payments which are made up of cost plus an agreed amount of profit and there is no element of interest included.

Types of Murabaha: Beyond the Basics

Murabaha is not a homogeneous type of transaction but it is a term that encompasses a variety of specific structures which are customized to meet specific financing needs.

Ordinary Murabaha (Direct Sale)

In the conventional murabaha, the bank buys an asset on behalf of the client and later sells it to the client at a price that reflects an agreed profit margin. This gain is predetermined and not subject to the current interest rates. The financing is most commonly used in the purchase of consumer goods such as automobiles, appliances and equipment where the bank buys the product through a dealer and the client purchases the item at a cost-plus rate.

Murabaha to the Purchase Orderer (MPO)

The MPO structure is the most common in the modern Islamic banking circles. It adds a step: the client places a purchase order with the bank, detailing the desired specifications. The bank buys the asset at the supplier and transfers it to the client with a profit margin that is given to the client. This structure is required to comply with AAOIFI Shariah Standard No. 8, and is traditionally used to make major transactions, including real-estate purchase and trade financing.

Commodity Murabaha

The financier is not given the particular commodity needed by the customer in commodity murabaha. Rather, it is sold to the customer who is buying a commodity, often a metal traded in the London Metal Exchange, and sells it straight away to a third party on a spot basis. The transaction then takes the form of cash-transfer.

The model raises scholarly concerns, because it is seen by some academics to be practically comparable to tawarruq, which is a mechanism limited by the Islamic Fiqh Academy (Jeddah). Since the commodity does not serve any real economic need of the buyer, as the only intention of the commodity is a cash transfer, the structure is approaching closer to a traditional loan in form.

For a related analysis of how Islamic scholars evaluate modern financial instruments, see our guide on whether Bitcoin is halal or haram.

Spot vs. Deferred Murabaha

Spot murabaha will enable the buyer to receive and pay for the asset immediately, commonly used in short-term halal trade financing. Deferred murabaha offers payment flexibility: the bank obtains the asset, makes a markup, and the customer pays in installments over a specified time. The deferred design is mainly used in financing of homes.

The scope of Murabaha is far beyond residential mortgages. The tool finds wide use in consumer financing, real-estate dealings, production, trade financing, letters of credit and import financing thus, it forms the staple of the entire international Islamic banking sector.

7 Common Misconceptions About Murabaha That Confuse Beginners

| Misconception | Reality |

| Murabaha is just interest by other means | It is not a loan; it is a real sale with a transition of ownership, sharing of risks, and an announced profit. |

| The bank does not really own the asset | Shariah doctrine requires genuine ownership and possession (qabd). The Prophet ﷺ taught: “Do not sell what you do not own” (Sunan Abu Dawud, 3503). |

| You can negotiate an early-payment discount | This is forbidden in advance, but the financier may, at his own discretion, forgive a part afterwards; this is not representable as a contract term. |

| Murabaha is the best type of Islamic finance | Conservative scholars view murabaha as a way of moving towards profit-and-loss sharing. Equity-based models such as mudarabah and musharaka are considered to be the best according to the Shariah perspective. |

| Penalty fees are tantamount to riba | Some scholars do allow obligatory penalty fees to be donated to charity; the price of the murabaha cannot appreciate. According to the Quran: “And if the debtor is in difficulty, then grant him respite until a time of ease” (Quran 2:280). |

| All murabaha are Islamic mortgages | Other structuring models like the ijara (lease), and the musharaka (partnership) are also structurally different. |

| Murabaha is specific to home financing only | The instrument is used in consumer finance, real-estate, production, trade financing, letters of credit, and import financing. |

For a complete understanding of Islamic financial obligations including zakat, see our dedicated guide.

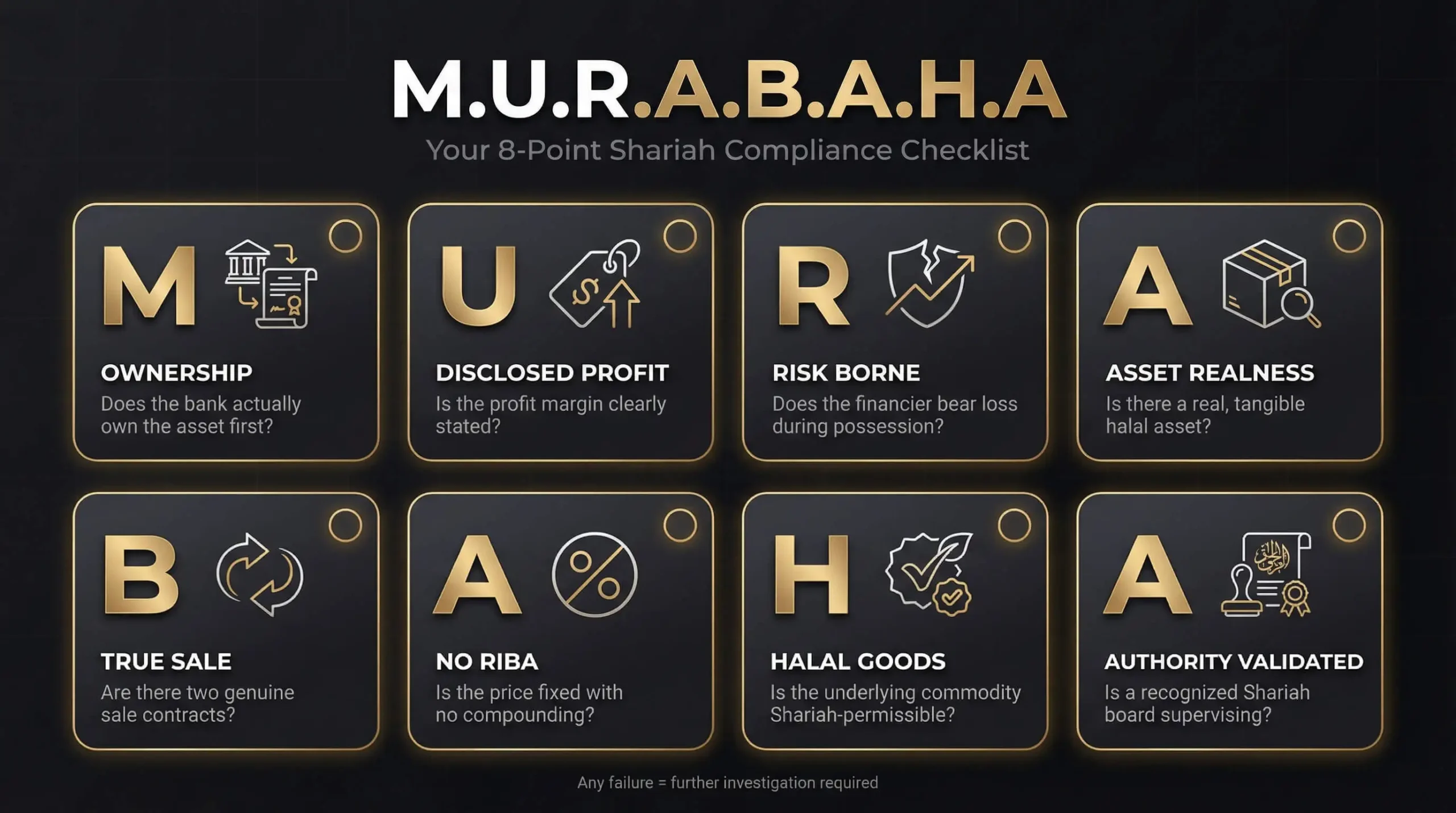

The M.U.R.A.B.A.H.A. Compliance Checklist — Your 8-Point Shariah Verification Tool

Before signing any murabaha agreement, take it to the following systematic framework. A different compliance criterion is coded in each of the letters:

| Letter | Check | Verification |

| M | Milkiyyah (Ownership) | Is the financier an actual acquirer and owner of the asset before its disposition? |

| U | Ujrah Muʿlanah (Disclosed Profit) | Does it clearly articulate and ratify the profit margin before it is executed? |

| R | Risk Borne (Risk Bearing) | Does the financier bear the possible loss or damage in its possession of the asset? |

| A | Asset Realness | Does it have a tangible, identifiable halal asset or is it a paper construct? |

| B | Bayʿ Authenticity (True Sale) | Are there two contracts, one on the purchase of the asset, and another on the sale of the same to the client? |

| A | Absence of Riba | Is the rate constant, no compounding or variable rate associated with traditional interest? |

| H | Halal Goods | Are you allowed to own the underlying commodity or asset under Shariah? |

| A | Authority Validation | Has the product been checked by a known Shariah board or approved scholar? |

Any lapse in these eight checks is a subject to prudential enquiries. A murabaha product which avoids the legitimate ownership, which hides its profit margin, or which uses a variable benchmark that is not acceptable according to the Shariah principles might fail to meet the conditions of validity.

The maxim of the default in transactions is permissibility (al-aṣl fi al-muʿāmalāt al-ibāḥah) can be applied to murabaha as a sale contract, assuming that no particular prohibition is forthcoming. The M.U.R.A.B.A.H.A. checklist helps verify that none of these prohibitions apply.

What the Quran and Hadith Actually Say About Murabaha: The Evidence Laid Out

For those seeking the complete textual basis, the following passages give the major sources of evidence which authorize, and also control, murabaha transactions, arranged in descending authority, as would have been the case in an academic syllabus.

The Quranic Foundation

One verse in Surah Al-Baqarah reframes the entire distinction between profiting from a sale and charging interest on a loan — and the reasoning is more surprising than you’d expect. The Quranic verse on which the permissibility of trade is based in all Islamic economies is the following:

وَأَحَلَّ ٱللَّهُ ٱلۡبَيۡعَ وَحَرَّمَ ٱلرِّبَوٰاْ

“Those who consume interest cannot stand [on the Day of Resurrection] except as one stands who is being beaten by Satan into insanity. That is because they say, ‘Trade is [just] like interest.’ But Allah has permitted trade and has forbidden interest (riba)…”

(Surah Al-Baqarah, 2:275)

When analyzing this text, Ibn Kathir draws the crucial line between legitimate business profit and the unlawful interest, and al-Qurtubi extends the definition of the trade, to include all consensual sales, such as the cost-plus and credit deals, on the condition that nothing about riba intrudes into the sale.

وَإِن كَانَ ذُو عُسۡرَةٖ فَنَظِرَةٌ إِلَىٰ مَيۡسَرَةٖۚ وَأَن تَصَدَّقُواْ خَيۡرٞ لَّكُمۡ إِن كُنتُمۡ تَعۡلَمُونَ

“And if someone is in hardship, then [let there be] postponement until [a time of] ease. But if you give [from your right as] charity, then it is better for you, if you only knew.”

(Surah Al-Baqarah, 2:280)

This verse is construed to be the main legislative principle of default policy in murabaha contracts. In the past, pre-Islamic Arab merchants could have insisted on either a cash payment or punitive interest rate, which Quran specifically prohibits. As a result, any late-fee which may figure in a murabaha contract should be donated to charity, and the cost of the contract should not be allowed to increase with time.

يَٰٓأَيُّهَا ٱلَّذِينَ ءَامَنُواْ لَا تَأۡكُلُوٓاْ أَمۡوَٰلَكُم بَيۡنَكُم بِٱلۡبَٰطِلِ إِلَّآ أَن تَكُونَ تِجَٰرَةً عَن تَرَاضٖ مِّنكُمۡ وَلَا تَقۡتُلُوٓاْ أَنفُسَكُمۡ إِنَّ ٱللَّهَ كَانَ بِكُمۡ رَحِيمٗا

“O you who have believed, do not consume one another’s wealth unjustly but only [in lawful] business by mutual consent. And do not kill yourselves [or one another]. Indeed, Allah is to you ever Merciful.”

(Surah Al-Nisaʾ, 4:29)

Other scholars, including Imam al-Shafiʿi and the Shafiʿi school of thought in general, understand this verse to make murabaha a kind of bayʿ al-amanah (trust sale). In this case, the consent and transparency are not only the desired ethical goals but also the essential legal and jurisprudential underpinning of the deal.

فَإِذَا قُضِيَتِ ٱلصَّلَوٰةُ فَٱنتَشِرُواْ فِي ٱلۡأَرۡضِ وَٱبۡتَغُواْ مِن فَضۡلِ ٱللَّهِ وَٱذۡكُرُواْ ٱللَّهَ كَثِيرٗا لَّعَلَّكُمۡ تُفۡلِحُونَ

“And when the prayer has been concluded, disperse within the land and seek from the bounty of Allah, and remember Allah often that you may succeed.”

(Surah Al-Jumuʿah, 62:10)

For a complete guide on how to pray in Islam, including step-by-step instructions, see our prayer guide.

This verse provides broad Shariah endorsement for profit-seeking through active trade — the very principle that underpins murabaha.

The Quran’s emphasis on patience during hardship is a recurring theme — see our collection of Quran verses about patience.

The Hadith Evidence

The Prophetic tradition confirms the permissibility of credit purchases: the Prophet ﷺ bought food grains on credit from a Jew and pledged his iron armour to him (Sahih al-Bukhari, Hadith No. 2068; also referenced as No. 2916 in some editions, Sahih). This narration confirms that the sale of deferred-payment is permissible, which is the foundation of murabaha.

Pre-sale ownership is compulsory: “Do not sell what you do not own” (Sunan Abu Dawud, Hadith No. 3503, Sahih). This simple yet profound injunction is the key to the necessary validity of any transaction that involves murabaha.

Possession earlier than resale is an obligation: “When you have bought something, do not sell it before you have taken possession of it” (Musnad Ahmad, Hadith No. 15399; Sunan al-Nasaʾi, Hadith No. 4613, authenticated by Sheikh al-Albani). This prevents entirely paper-based murabaha transactions in which the bank does not actually possess the asset.

Another statement of the Prophet ﷺ is, he prohibited selling goods in the same place where they were bought before traders transport them to their own destinations (Sunan Abu Dawud, Hadith No. 3499). This explains why physical transfer and possession are necessary.

Classical evidence: “Whoever purchases food, let him not resell it until he has taken full possession of it” (Narrated by Ibn ʿAbbas; Sahih al-Bukhari, Hadith No. 2126; Sahih Muslim, Hadith No. 1525, Sahih). This hadith further reinforces the requirement of possession.

Prophetic precedent to credit transactions: The Prophet ﷺ had transacted credit-purchase transactions and had also paid back more than the original. This helps to substantiate the principle of murabaha in its fullest form when it is a real trade and not a finance charge.

The fiqh maxim of la darar wa la dirar (no harm, no reciprocating harm) demands transparency; the publicly visible cost-plus system will ensure the purchaser is not exploited and will ensure the legitimate component of gain is enjoyed by the seller instead of eliminated.

Recent Developments: Murabaha in 2025–2026 — What’s Changed

Over the past years, the murabaha landscape has also experienced radical development.

AAOIFI Standards Reform Debate: An academic study, authored in 2025 by Bhatti, Saleem and Mansor, revealed that speaking of the arrangement fee in clause 2/4/4, Pakistan Islamic banks fail to adhere to AAOIFI Shariah Standard No. 8 in full. The study also revealed discrepancies between Standard No. 24 and Standard No. 8 — bringing doubts to the consistency of implementation in different jurisdictions.

AAOIFI Standard 59 (Sale of Debt): The introduction of the AAOIFI Shariah Standard No. 59 covering the sale of debt has been the catalyst of a significant market re-organization of murabaha financings specifically in the UAE and the Gulf market. Banks have been forced to change their way of handling murabaha receivables.

AAOIFI Standard 62 (Sukuk): While AAOIFI indicated in early 2025 that Standard 62 could be approved that year with a one-to-three-year implementation window, as of early 2026 the standard remains in the amendment phase with no confirmed finalization date. Although it specializes in sukuk, its larger agenda reflects the trend within AAOIFI towards compliance with authentic Shariah, with effects on the design of instruments being issued under murabaha. Separately, AAOIFI’s ongoing accounting standards reform is expected to supersede FAS 2 (Murabaha and Murabaha to the Purchase Orderer) and FAS 20, though this is a distinct process from the Shariah Standard 62 sukuk framework.

U.S. Market Expansion: Devon Bank currently serves 34+ states, and Guidance Residential and UIF Corporation service the other states. Halal Islamic mortgage home financing is becoming more available geographically.

Morocco: Since 2017 participatory banks have been providing murabaha-based real-estate contracts, including Umnia Bank, CIH Dar, and Al Akhdar Bank. These products are attractive to an increasing number of borrowers who will be inspired by their religious beliefs and need to understand their financial structures in a more transparent way by 2026.

There Will Be No More LIBOR: Even some older sources still refer to LIBOR as the standard in making murabaha. In June 2023, LIBOR was completely abolished. Modern murabaha rates are SOFR (Secured Overnight Financing Rate) in the United States, SONIA in the United Kingdom or IIBR (Islamic Interbank Benchmark Rate). The fiqh principle is al-maʿruf ʿurfan ka al-mashrut shartan (that which is customary is akin to that which is stipulated) which legitimizes the application of market benchmarks as ʿurf in determining prices, without making the profit rate of a murabaha identical to interest.

Academic Debate on Commodity Murabaha vs. Tawarruq: The scholarly debate on the topic of commodity Murabaha, specifically its use to generate liquid assets is still under critical examination. Position papers have been issued by major Islamic jurisprudence institutions like the Islamic Fiqh Academy of Jeddah and the Assembly of Muslim Jurists of America (AMJA) and continuing control over this area has been maintained by the Fiqh Council of North America.

For readers exploring other financial instruments under Islamic law, our analysis of whether forex trading is halal examines similar Shariah principles.

Frequently Asked Questions About Murabaha

Is murabaha halal?

The four Sunni madhabs — Hanafi, Maliki, Shafiʿi, and Hanbali — endorse murabaha as permissible when its conditions are strictly met. The Quranic command in Surah Al-Baqarah 2:275 mandates trade and forbids riba. Murabaha is classified as a genuine sale, not a loan. Any murabaha contract must satisfy the five Shariah conditions to be valid. Allah knows best.

For a foundational understanding of what Islam is and its five pillars, see our complete guide.

In simple terms, what is the meaning of murabaha?

Murabaha is an Islamic financing whereby the financial institution obtains the article which the customer would like to buy and then sells it to the customer at a transparently disclosed higher price consisting of the purchase consideration plus a fixed profit. The client pays in agreed instalments; no interest is involved, it is just a sale and a set markup.

What is the difference between a conventional mortgage and murabaha?

A traditional mortgage pays out capital to the lender in form of interest. Murabaha requires the bank to take possession of the property initially, then sell it to the borrower at a marked-up price. The risk is transferred to the owner during the ownership period; the bank makes profit based upon the sale rather than lending.

What is Devon Bank murabaha?

Devon Bank buys the property that the client chooses, and sells it to the client on a fixed-price agreement. At closing, the client never enters into a promissory note showing principal and interest; rather a murabaha contract on the remaining value is signed. Devon Bank has implemented this model since 2003 in more than thirty-four states within the United States.

Are there any costs in case of late payment?

No. The set contract price cannot be changed in case of default. Some jurists will permit a fine to be paid to charity, but not the price of the contract itself. This ban is one of the fundamental characteristics that differentiate murabaha from riba.

Does it mean that murabaha is tawarruq?

No. In murabaha the client is given a real asset to be used. In tawarruq, the bank sells a commodity to the customer who sells it instantly on the exchange to get liquidity — therefore, similar to customary lending in format. Tawarruq is treated with greater scrutiny by various scholars.

What is commodity murabaha?

Commodity murabaha involves a situation where the financier purchases commodities, usually metals, and sells them to the customer who resells the commodity to a third party at spot. It is a tool common in interbank and treasury dealings as opposed to consumer funding.

Which is the best Islamic mortgage model in USA?

The U.S. market has largely adopted musharaka (diminishing partnership) as a model of choice for its regulatory compatibility. Still, murabaha remains popular through institutions like Devon Bank. The best alternative depends on fixed-price certainty versus equity partnership.

Is AAOIFI dealing with murabaha?

Yes. Murabaha to the Purchase Orderer is subject to AAOIFI Shariah Standard No. 8. AAOIFI has created a complete framework of Shariah-compliant structures — including murabaha, musharaka, ijarah, and sukuk — which Islamic financial entities use globally.

Is it permissible to use murabaha financing by non-Muslims?

Indeed. Halal mortgage service is available to people regardless of religious beliefs. Some non-Muslim customers willingly choose Islamic financing for the fixed-price certainty which removes variable rates and fully reveals the overall cost.

Is Murabaha Right for You?

Murabaha stands at the convergence of Shariah compliance and pragmatic finance. It is a true sale contract which is based on the Quranic approval of trade and under the conditions of ownership, possession and transparency developed by Hadith and universally accepted by the four Sunni madhabs. Meanwhile, its principal academics consider it a second-best option compared with ownership-based systems like musharaka and mudarabah, which more fully embody Islam’s spirit of shared risk and reward.

The decision-making in relation to murabaha primarily concerns evaluation between three factors: (1) whether the given product corresponds to each of the elements of the M.U.R.A.B.A.H.A. compliance checklist; (2) whether the given fixed-price structure is more suited to your financial strategy than partnership or lease ones; and (3) whether the product is overseen by a recognized and credible Shariah board.

The article is aimed at education only. To be advised on a case-to-case basis, a registered Shariah advisor should be consulted. Allahu Aʿlam.